Resources for Understanding the Russian Economy

Analysis and preparation by Maxwell Scott

Introduction

An analysis of the Russian economy has to begin with the context of the present conflict in Ukraine and the impact of sanctions on Russia. It should be recalled that some sanctions from the days of the Soviet Union continued afterwards, most notably sanctions on technology considered to have military implications, including on microchips. There is an ongoing tacit assumption in the West that Russia does not have a microchip industry but of course it does and the last time that I looked it could make chips at 7 nanometres. At that time it was known that China could make them at 9 nanometres. Now with the new Huawei phone, it is known that China can do 5 nanometres, and there is further information about Russian capabilities but these will not be discussed here.

These sanctions were augmented by additions following the Maidan coup of 2014 and the subsequent voluntary re-integration of Crimea into Russia, following a referendum run by the Russian government. However, contrary to Western claims that this was fixed, that referendum produced an almost identical result to a referendum held a few years earlier under Ukrainian rule, which was then echoed by a vote in the Crimean Rada (regional assembly). Both referenda had large majorities of about 80 per cent favouring a return to Russian rule. Russia justified the reintegration of Crimea under the UN Charter’s recognition of the right to the self-determination of peoples.

The post-Maidan government almost immediately passed a law removing recognition of Russian as an official language of Ukraine, and in anticipation of probable consequent unrest in eastern Ukraine, especially in the Donbass, the interim President sent troops to attack there. (He subsequently admitted that he had ordered this.) People in the Donbass managed to organise resistance to this, and the resulting fighting lasted right into the beginning of the Special Military Operation [SMO], thereafter continuing with Donbass militias being integrated into the Russian Armed Forces.

It is now confirmed that while Russian government forces did not intervene during the years 2014 – 2022, Russian military supplies and equipment were facilitated by the Russian government, and this is probably when the Wagner Group was formed under Prigozhin as a plausibly deniable figurehead. He was answerable to the GRU [Russian military intelligence] with the operational commander being Dmitry Utkin, who remained a member of the GRU, but it seems that oversight was not close, and this enabled a culture of relative impunity and opportunism to develop, especially when Wagner moved into Africa. It should be stressed that Wagner has always been a group of storm troopers, however large and well-equipped, and it seems that it was not formally trained in Russian Ministry of Defence military doctrine or methods of developing strategy, or indeed operational decision-making. That ‘cognitive dissonance’ presumably led to the various famous disagreements, especially during the battle for Bakhmut/Artyomovsk. Consequently, Wagner has never been all that important to the Russian Ministry of Defence, but apparently did not understand this. It did have good social media skills which bolstered its popular support. It was formally disbanded after Prigozhin’s death. However, a successor organization that is fully integrated with the Russian Armed Forces has now been formed with some of the previous staff.

The present SMO conflict came about after mid-December 2021 when Russia proposed a new security architecture for Europe that required NATO to return to its 1997 borders and to remove Aegis Ashore missile batteries from Romania and Poland. These proposals were ignored and then effectively rejected by mid-January 2022. In early February 2022, the Armed Forces of Ukraine [AFU] which had been built up over the years to be the ‘ second largest armed force in NATO after the USA ’ (but not officially) started a much-increased artillery barrage against the Donbass. President Biden had already declared confidently that Russia would invade Ukraine, presumably because he knew that it could be forced to do so if the AFU posed a serious enough threat to the Donbass.

However, the extensive AFU fortifications along the line of contact in the Donbass had been built on the assumption that Russia would attack them from the Donbass, and so it was a surprise when the Russian attack mainly came from the north and south of Ukraine, and not the southeast. The other surprise was that Russia only attacked with about 200,000 soldiers, whereas conventional wisdom had it that a successful strategic attack should have a numerical advantage of three to one, not a much smaller force than the AFU. Since then, NATO strategists and politicians have consistently misunderstood Russian intentions and strategy. Both have changed over time, but these changes have been completely misinterpreted, with the result that the AFU and NATO have now been seriously weakened because they failed to adapt to the changes in the Russian strategy. Yet even though it is now partly understood in NATO that for Russia this a ‘war of attrition, not of manoeuvre’ the relative capabilities are still not fully understood in Western political, military and ‘think tank’ circles. It is not the purpose of this paper to elaborate on this point. It has been well analysed by retired Western military and intelligence personnel if one cares to look for those sources.

There are three main reasons why NATO got it so wrong about the conflict in Ukraine:

Firstly, as Ray McGovern and Larry Johnson have pointed out, Western intelligence agencies, especially the CIA and MI6, stopped engaging in open source analysis. As McGovern has stated, it used to be 80 per cent of the job. Ray McGovern has also stated that this new approach started in earnest with the Clinton Administration, while Larry Johnson has added insights about how pressure to rewrite analyses to suit the audience further up the hierarchy was already operating while he was in the CIA from 1985 to 1990.

Secondly, Operation Desert Storm in Iraq in the early 1990s was a major military success with limited resources, but with air cover, and with two very competent mid-level officers who made sure that vital elements in the strategy were made to work. These were Col. Douglas MacGregor, US Army, and Major Scott Ritter, US Marines. MacGregor was a tank commander who was involved in the preparation of the overall strategy (having learned the importance of intensive training while living for a year in Germany) and having also been involved in preparing the physical ground for subsequent forces to arrive in Iraq. He was also responsible for the US victory in the largest tank battle since WW2 when his tank force unexpectedly encountered the bulk of the Iraqi tanks and defeated them all very quickly, thereby proving again the importance of thorough training in sustaining quick reactions under fire. Ritter was trained in computer modelling of battlefield scenarios and worked very hard ‘running the numbers’ for the US Marines until he was sure that they would be able to take the town that was their objective, which they did two days early, to the fury of the overall commander General Schwarzkopf. The result of this first dramatic US military victory since the Vietnam war was that people thought that this expeditionary war against a poorly trained adversary that lacked adequate air cover was the modern way to conduct war. MacGregor knew full well that this was nonsense, but his opinions differing from the new groupthink were suppressed, and his career was effectively over.

Thirdly, the US and UK in particular had already started the financialization of their economies and offshoring of their industry (mostly to China) in the 1980s and the resulting cheap imports further enabled their ongoing de-industrialisation. Consequently, after the end of the Soviet Union, this groupthink seemed to show that Western global hegemony had a long, rosy future. Western university centres studying the Soviet Union and Eastern Europe were closed down. These included most notably the Centre for Russian and East European Studies [CREES] at the University of Birmingham, Le Centre d’Economie Internationale des Pays Socialistes [Universite de Paris 1, Pantheon-Sorbonne] and the Institute of Soviet and East European Studies at the University of Glasgow. (The London School of Slavonic Studies was not in the same league and neither were similar institutions in the USA. Harvard University mostly focussed on Soviet history and politics.)

In the UK, there was also the considerable expertise on the Soviet military, and on science and politics at Edinburgh, under the direction of Professor John Erickson. This was complemented by the political analysis of Professor Archie Brown at St. Antony’s College Oxford, but as a result of the downplaying of the apparent importance of post-Soviet Russia any high quality research that took place subsequently was by relatively isolated individuals such as Professor Richard Sakwa at the University of Kent.

These trends were not mitigated by people with relevant expertise who had lived and worked in the Soviet Union, and retained an interest after it ceased to exist. In part, the lacunae in their knowledge and understanding were a result of a successful post-Soviet Russian policy of continuing to hide very important military research, while sustaining such capabilities on very limited budgets. This approach of hiding Russia’s strengths became more widespread when Evgeny Primakov became Foreign Minister in 1995. Consequently, such people as Scott Ritter, who had been trained on the Soviet Union including learning Russian while in the US Marines and had spent over two years from late 1987 to early 1990 working on arms limitation in the Soviet Union and monitoring the implementation of the Intermediate Nuclear Forces [INF] Treaty, had no knowledge of the existence from the late 1970s of networked supersonic cruise missiles capable of sinking ships. It has taken the three books and blogs of Andrei Martyanov to point this out.

Yet we now know that by 2004 Russia had quietly informed the USA that it was starting to develop new weapons technology, and some of these proposed weapons were outlined at that time. Putin’s famous speech at the 2007 Munich Security Conference angered many in the West, but it was still not taken seriously. Consequently, when Putin announced a suite of next-generation weapons in March 2018, the US response was (a) yes we already knew about some of these and (b) this is really all bluff and bluster.

This reaction indicated how deep the malaise of cancel culture already was. Putin’s speech in 2018 was an announcement that the USA had lost an arms race that it did not know was happening. Yet incredibly the cancel culture then worsened to the point where the US Defence and Intelligence Agency [DIA] was excluded from decisions about the conflict in Ukraine and the US Federal Reserve was excluded from the decision to exclude Russia from the SWIFT system of international payments. SWIFT then lost about 30 per cent of its business, and global trust in Western financial institutions dwindled more rapidly than the collective West understood. Presumably the Fed knew that Russia had already developed an alternative system of international payments, and in response Russia simply scaled up its usage of that. [The DIA is now back in the decision-making process, but at the cost of adhering to the consensus.]

This Western culture of denial is now confronted with the fact that it has recently been announced that the Sarmat nuclear ICBMs, with a range of 18,000km, are now fully in service. They could actually go over Antarctica on their way to attacking the USA. All of the other weapons apart from the Burevestnik announced in March 2018 have been deployed too, plus some others that were previously unknown, and overall the Russian armed forces had their equipment modernised in all areas by about 73 percent between 2010 and 2021. The modernisation proportion has been higher than that average (about 82 percent) in the most high-tech weapon systems. That in itself implies considerable economic and technological capacity. Yet still Russia is widely seen as incapable of defeating Ukraine, let alone the whole of NATO. That is why it is now important to assess Russian economic structure, functioning and capacity, including its capacity for innovation.

Attempt at a Rational Appraisal

An important attempt at such analysis by the Swedish economist, the late Jon Hellevig, was published on the website of the Awara Group, which he then headed, in 2018.

https://www.awaragroup.com/blog/russian-economy-strong-and-stable/

Regrettably, he died of COVID-19 in 2020, but the consultancy group lives on and one can see that there are another 44 articles, many by Jon Hellevig, on the right hand side of the web page.

Hellevig argued that the Russian state was less dependent on hydrocarbons than was generally assumed. While most estimates put the proportion of oil and gas taxes in the state budget as being over 30 percent, he estimated that it was about 23-25 percent. That may have been a bit low as an estimate, but he was surely right to imply that the proportion of tax income from hydrocarbons would vary depending on the scale of other forms of economic activity. Those other forms will grow, perhaps more than proportionately, as the economy grows, and it is now about double the size that it was in the year 2000. He also stressed that Russia had a lot of scope for increased returns on investment in infrastructure, pointing to the fact that since the year 2000 18 bridges over 10km long had been built, more than at any other time in Russian history.

This trend has continued with the recent completion of the rail bridge over the Amur River/Black Dragon River between Russia and China:

“The first freight train from China arrived in Russia via the railway bridge across the Amur

The bridge links the Jewish Autonomous Region and Heilongjiang Province. In just eight months since the launch of the bridge, over 1.6 million tons of cargo have been transported from Russia to China.

The new corridor allows for reducing the distance of cargo transportation to the northern provinces of China by more than 700 km compared to existing routes.” (Reuters, 29 July 2023.)

That bridge has very long sidings on the Chinese side to facilitate the transfer of wagons/carriages from the Russian gauge to the Chinese gauge. Other smaller road bridges are being completed, such as a new bridge across the Volga near Samara and Togliatti. To some extent such construction is being increasingly prioritised in terms of where it would fit in with the policy objectives of the Eurasian Economic Union [EAEU] and the Belt and Road Initiative [BRI]. These two economic strategies are now formally aligned.

Hellevig argued in effect for the resilience of the Russian economy, and this was already evident when the first major sanctions were placed on Russia in 2014 following the conflict that started after the Maidan coup in Ukraine in February 2013. Putin argued in 2014 that Russia would recover from those sanctions in 18 months and that is precisely what happened. Similarly now one can see below from the statistics that Russia has recovered from the sanctions imposed in 2022, and indeed at both times the sanctions seem to have made it easier to make changes that would otherwise have been politically difficult.

The Relative Size of the Russian Economy

From the IMF World Economic Outlook April 2023, one gets this impression of the relative size of the 8 largest economies, calculated by the IMF in ‘International Dollars’ using an implied Parity Purchasing Power [PPP] conversion rate:

GDP Purchasing Power Parity, Billions of International Dollars, IMF April 2023.

China, People’s Republic of: 33.01 thousand

United States 26.85 thousand

India 13.03 thousand

Japan 6.46 thousand

Germany 5.55 thousand

Russian Federation 4.99 thousand

Indonesia 4.40 thousand

Brazil 4.02 thousand

Source: https://www.imf.org/external/datamapper/datasets/WEO

Within that link, this is the specific source to check, looking for the box ‘GDP, Current Prices, Purchasing Power Parity, Billions of International Dollars’:

https://www.imf.org/external/datamapper/PPPGDP@WEO/OEMDC/ADVEC/WEOWORLD

Note: A thousand billion Dollars equals 1 trillion Dollars, but most economies do not reach that level, staying in the billions, which is why this table uses ‘thousand’ for those that are over 1 trillion Dollars.

All the countries in these tables are listed in alphabetical order in this source, including ones with ‘no data’, so this order of economic magnitude is not immediately apparent. Four of these 8 economies were founder members of BRICS.

[There is a separate table giving the dollar conversion rate for each country to show what an implied PPP is. It is called ‘Implied PPP Conversion Rate’:

https://www.imf.org/external/datamapper/PPPEX@WEO/OEMDC/ADVEC/WEOWORLD]

For what may be the first time ever, this GDP-PPP comparator rates China as being a larger economy than the USA. I have not noticed any commentary on this, which is surprising given that the size differential is almost as large as the size of the Japanese economy at 6.16 trillion. That’s almost 23 per cent larger by this measure.

Yet Russia is still rated as being smaller than Germany, which is surprising given how well Russia is doing partly because of (rather than despite) sanctions. However, the IMF may well underestimate both Russia’s relative size and its capacity for growth.

The IMF forecast of Russian growth for 2023 is surprisingly low:

- 2023 Projected Real GDP (% Change) : 1.5*

- Country Population: 143.204 million

- Date of Membership: June 1, 1992

- Article IV/Country Report: March 28, 2023

- Special Drawing Rights (SDR): 17365.55 million

- Quota (SDR): 12903.7 million

- Number of Arrangements since membership: 4

*GDP Data from July 2023 World Economic Outlook Update

Source: https://www.imf.org/en/Publications/WEO/Issues/2023/07/10/world-economic-outlook-update-july-2023.

This forecast of real GDP growth is presumably controlling for inflation. In fact, the graph of real GDP growth in the Article IV/Country Report cited above shows a graph of growth rising to 0.7 per cent by mid-2023, with a forecast of a slight further growth and then growth slowly declining afterwards, but there is no obvious explanation or evidence for these estimates. This suggests that there was a tacit assumption that Russian economic growth would be at least halted by economic sanctions. If there was, such an assumption was evidently wrong, as will be seen below. In previous reporting, the IMF had underestimated Russian growth and so had then accepted the Russian government forecast, but in 2023, the estimate seems to be no longer based on Russian estimates, despite the latter having a good track record. This apparent assumption of very low economic growth seems to have been operative since the beginning of 2023:

https://www.imf.org/en/Publications/WEO/Issues/2023/01/31/world-economic-outlook-update-january-2023

This forecast 0.3 per cent for Russia in 2023, and indeed the forecast for Russia in October 2022 was for minus 2.3 per cent. Here is a report confirming that this really was what the IMF believed at mid-April 2023:

https://www.intellinews.com/imf-improves-russia-s-2023-gdp-forecast-from-0-3-to-0-7-275604/

12 April 2023.

However, a very detailed IMF spreadsheet including data on Russia has no data for Russia beyond 2021. This spreadsheet is called ‘WEOApr2023all’. It seems that no data on Russia has been collected since the start of the SMO, despite Russia being a member of the IMF.

A recent forecast by the Russian Finance Minister for growth this year was 2.5 per cent Year-on-Year [YOY] with inflation staying at about 6 per cent:

https://tass.com/economy/1665831

26 August 2023. Other evidence on Russian growth will be discussed later.

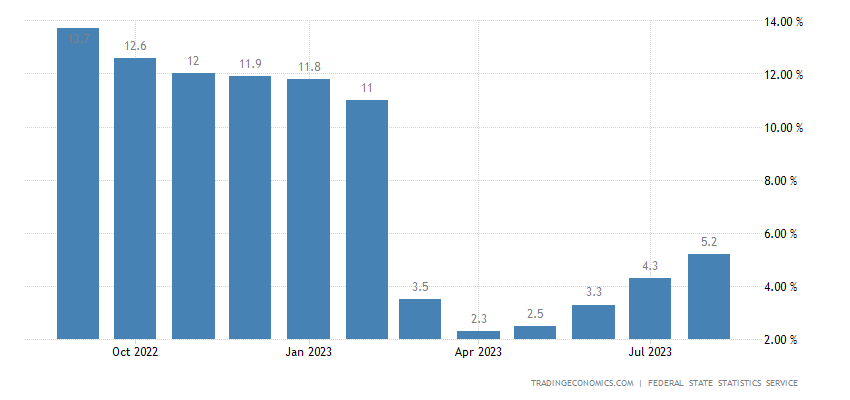

Inflation

The Central Bank of Russia [CBR] has inflation for August 2023 at 5.2 per cent, and the interest rate at 12 per cent was changed to 13 per cent on 18th September. Its target for inflation this year is 4 per cent but despite the success in reducing inflation from 14 per cent last year, it cannot be assumed that the 4 per cent target will be reached by year end:

https://cbr.ru/eng/key-indicators/

From this source on 8 September 2023, the international reserves of the CBR on 1st September 2023 were 576.6 billion US Dollars. [Definitions of various kinds of loans and debt at the CBR are not readily accessible on the above website.] These reserves are the foreign currency reserves held by the CBR, and not the reserves held by various Russian wealth and direct investment funds. Those will be discussed later.

What the size of these international reserves strongly suggests is that the CBR was indeed successful at repatriating the overwhelming majority of its reserves held abroad before they were frozen under Western sanctions. There was a report claiming that about 90 per cent of the $330 Billion held in foreign financial institutions was recovered. If this was true, then the collective West not only failed to impose its main financial sanctions, but also persuaded a lot of the Global South that Western banks could not be trusted as a safe haven. This apparent loss of trust may be fuelling the process of de-dollarisation.

Now, the CBR’s figure for inflation is identical to that of the Federal State Statistics Service, and this source gives a clearer picture of changes in the rate of inflation in 2022-3 so far:

https://tradingeconomics.com/russia/inflation-cpi

Here are the details:

The annual inflation rate in Russia rose to 5.2% in August 2023 from 4.3% in July, marking the highest level in six months and above market expectations of a 5.1% increase. The central bank has indicated its potential interest rate hikes this year, aiming to bring prices back to its 4% target by 2024, as it predicts that inflation will likely range between 4.5% and 6.5% by the end of this year. Prices saw accelerated increases for food (3.6% vs. 2.2% in July) and non-food products (3.6% vs. 2.3%). Conversely, services inflation slowed to 9.5% from 10%. Meanwhile, core consumer prices accelerated (3.95% vs. 3.2%). On a monthly basis, consumer prices increased by 0.28%, following a 0.6% rise. source: Federal State Statistics Service

In the light of this evidence, it is possible to see how the Finance Minister’s forecast of inflation being 6 per cent Year-on-Year is accurate, but that conceals the dynamics shown by the histogram, namely that inflation has been well below that average from April till August 2023. Even though inflation is rising again, the month-on-month [MOM] index is falling slightly:

https://www.statbureau.org/en/russia/inflation

This shows that the MOM index was 0.63 per cent in July and 0.28 per cent in August. Consequently, the recent increase in the interest rate to 13 per cent may seem somewhat restrictive. Overall, it is clear that inflation had been largely brought under control despite the dislocation resulting from the SMO. However, inflation has picked up further in recent days:

https://tass.com/economy/1684689

4 October 2023. Russia’s annual inflation accelerates to 5.94% on September 26-October 2.

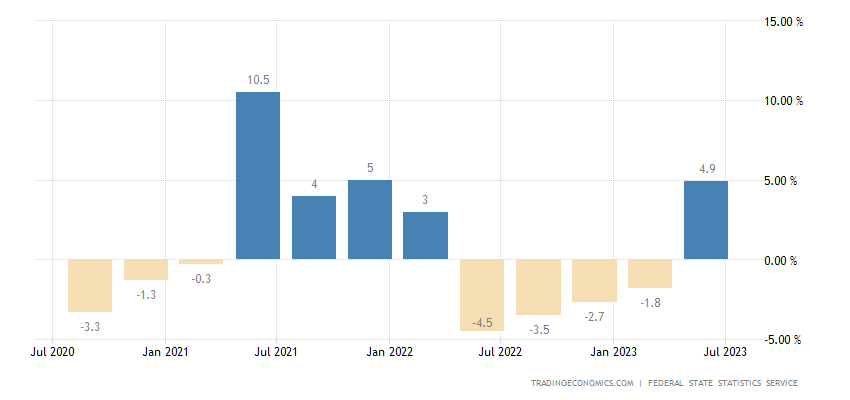

Economic Growth

This is the general situation:

https://tradingeconomics.com/russia/gdp-growth-annual

Russia’s gross domestic product sharply increased by 4.9% year-on-year in the second quarter of 2023, recovering from a 1.8% contraction in the previous period and aligned with the preliminary estimate. Notably, it marks Russia’s first GDP expansion since the first quarter of 2022, when the nation’s invasion of Ukraine led to international sanctions. The expansion is seen as a positive sign by the Central Bank of Russia, indicating a recovery in domestic demand and foreign trade from the shocks of Western sanctions, strengthening the case for interest rate hikes. The sectors contributing to GDP growth include agriculture, forestry, hunting, and fishing (4%), manufacturing industries (10.6%), construction (11.7%), wholesale and retail (11%), hotels and restaurants (15.2%) and activities in the field of information and communication (3.5%). On the other hand, the economy contracted for health and social services (-3.2%) and water supply, sewerage, and wastewater disposal (-1.7%). source: Federal State Statistics Service

The negative growth rate for the second half of 2020 is related to COVID-19, with a bounce back in the second quarter of 2021 and then a reasonable growth of around 4.5 per cent for the third and fourth quarters of 2021. Even the first quarter of 2022 showed growth at 3 per cent before becoming negative from then until the fourth quarter of 2022. This negative growth continued in the first quarter of 2023 with minus 1.8 per cent, but then it recovered to a positive 4.9 per cent in the second quarter. That means that overall the Russian economy grew by roughly 3.1 per cent in the first six months of 2023.

The time series of growth from January 2019 to August 2023 can be found here:

https://www.statista.com/statistics/1009056/gdp-growth-rate-russia/

This shows that the rate of growth in August 2023 was 5 per cent. Consequently, the IMF forecast for Russian growth of only 1.5 per cent for the whole year in the World Economic Outlook of July 2023 looks decidedly pessimistic in the light of this evidence.

Here is a commentary on the changing Russian approach to economic growth that no longer follows IMF orthodoxy:

31 January 2023.

The sectoral pattern of growth so far in 2023 hardly suggests a total transfer to a war economy. Only a couple of sectors contracted. That is surely indicative of a remarkable resilience. Since then, there have been indications that military industrial production has been growing rapidly, especially in tanks and other armoured vehicles, and a whole variety of drones, whose uses on the battlefield have diversified rapidly. This is doubtless related to the massive ongoing recruitment of personnel for the armed forces, with around 280,000 reservists recruited in the autumn of 2022, plus an additional 300,000 volunteers, of which about 20,000 were recruited along with the reservists.

This recruitment has exacerbated an already existing labour shortage, which has been partially offset by recruiting personnel from Central Asia. Controversially, this has included people previously deported after being released from Russian prisons, and there has evidently been sentiment against this. There have been quiet roundups and deportations of foreigners who have exhibited criminal or unacceptable behaviour, although the extent of this is unclear. Presumably at least some of the more than 2 million refugees from Ukraine have also eased the labour shortage.

Commercial banking also showed resilience:

https://tass.com/economy/1567929

27 January 2023. Russian banks’ profits in FY 2022 were almost $3 billion. [Thus $5 billion profit for December 2022 means that earlier debts were nullified by later profits.] Meanwhile foreign banks were closing their Russian offices:

https://tass.com/economy/1571227

3 February 2023. Ten representative offices of foreign banks shut operations in Russia in 2022 — regulator.

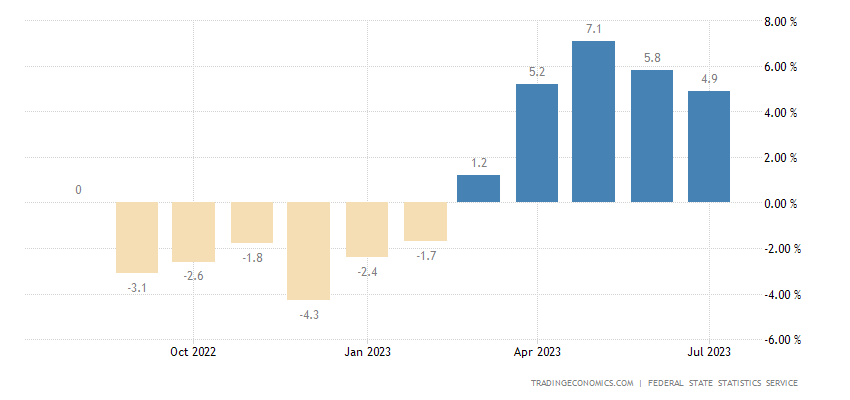

Industrial Production

https://tradingeconomics.com/russia/industrial-production

Industrial production in Russia rose 4.9 percent year-on-year in July 2023, easing from a downwardly revised 5.8 percent advance in the previous month and compared with market expectations for a 5.1 percent increase. Output eased for manufacturing (9.5 percent vs 11.8 percent) and continued to fall for extraction of raw materials (-1.5 percent vs -2 percent). On the other hand, production rose faster for electricity, steam, and air conditioning (2.7 percent vs 2.2 percent) and water supply, wastewater disposal, and the collection and organization of waste (8 percent vs 3.1 percent). Considering the January-July period, industrial activity rose 2.6 percent. source: Federal State Statistics Service

It is not clear how the apparent growth for water supply, waste water disposal and the collection and organization of waste relates to the claim of contraction in this apparently same sector in the discussion above, but presumably there was a contraction in water supply etc. in other parts of the economy, perhaps with a prioritisation of water supply etc. for military industrial production. Yet the overall pattern of growth from March to July 2023 is clear.

This is corroborated by the Purchasing Managers’ Index [PMI] (source, Slavyangrad Telegram channel, 4 September 2023):

“PMI or business activity index. The Russian manufacturing PMI for August 2023 was 52.7. That’s over 50, which means that their purchases are up. New orders rose to a three-month high. By contrast, the EU manufacturing PMI was only 43.7. So Russian economic growth prospects are improving, while those of the EU are declining, since a score of 50 presents ‘no change’.”

From the above graph, one can see the dramatic declines after the Global Financial Crash of 2008, and during the outbreak of COVID-19. One can also see the decline during the sanctions of 2014, and the rapid recovery followed by a lower level of activity and a rise again over 2017-8. After the COVID-19 outbreak, activity returns more or less to previous levels and fluctuates more again during the SMO. It stays above 50 in late 2021 but declines sharply in early to mid-2022. The subsequent rise is doubtless owing to military industrial production, at least in part, but it is clear that by September 2023 civilian production is also playing a role as new models of cars come on to the market, for example. Civil aviation is also receiving new versions of passenger jets (the SU-SJ and the MS-21) that have no foreign components – a rapid adaptation to sanctions. This experience is now being applied to the new wide-bodied passenger jet currently being developed.

Slavyangrad, 3 June 2023. [Slavyangrad is a Telegram channel, henceforth designated a ‘S’.]

Unmanned KAMAZ trucks started regular cargo transportation in the Arctic

It’s not just testing anymore. The trucks transport Gazprom Neft’s cargo daily along a 140-kilometer winter road in hard-to-reach areas of the Yamalo-Nenets Autonomous District.

Each drone is equipped with an array of sensors that scan the environment, recognize obstacles within a 200 meter radius, and create a digital road map. The software is entirely Russian.

On busy roads, traffic is also possible – they are currently being tested in different cities of Tatarstan. [end.]

KAMAZ BROKE THE LOCALIZATION RECORD

KAMAZ continues import substitution of components, which became unavailable due to the sanctions. Today the localization of K5 generation trucks is more than 70%. More than two thousand components are Russian. This exceeds the average figure in the world practice of truck manufacturing – usually it is about 60%. KAMAZ buys some highly complex components from partners in friendly countries.

The plant is planning to bring the level of localization of production to 100%, and produce all components, including currently imported ones, independently. Today the suspension and engine parts, the cab, seats, climate control, windshield wipers, hatches, air intakes, hinges, window lifters, door locks, as well as steering column brackets and a number of other things are localized.

The sanction-resistant cars feature reduced fuel consumption, improved noise isolation, modified interior screens and dashboard, and increased service intervals. [end.]

A new factory will be built in Russia for mass production of space satellites.

Since 1957, every satellite has been assembled by hand, there has never been mass production. But now there is a demand not only for scientific or military, but also for commercial launches. The demand is massive, so it is necessary to automate all processes.

All Russian enterprises put out a total of 15 satellites a year, and with some modernization this number can be increased to 42, but Roskosmos says that the demand is much higher. The medium-term goal is to assemble one satellite per day.

Now a site is being chosen, the first plant will be built either in the Moscow Region or in the Krasnoyarsk Territory. [end.]

Tatarstan is starting to produce Russian diesel engines for cars.

The manufacturer, Sollers, used to assemble cars for Ford, Mazda and Aurus, and since last year it has been producing its Argo and Atlant mini-trucks. The first engines of 2.7 liters will be installed on them. There are also plans to put two-liter diesels on UAZ cars.

In the future, the plant is ready to produce engines for agricultural machinery, machinery, and shipbuilding. [end.]

However, foreign companies are still leaving Russia:

https://tass.com/economy/1586131

8 March 2023. German tire manufacturer Continental announced plans to leave Russian market.

A real import substitution boom. Since the beginning of the year, production of clothing in Moscow has increased by 95% and footwear by 58%.

This is an increase on last year, which was already a record for the capital’s light industry.

In general there are about 250 enterprises in the city, which produce clothes. Among them are both factories with a long history (for example, Bolshevichka) and ultra-fashionable brands like Outlo, which are quickly occupying the niche of the foreign brands which have left. [end.]

In addition, innovation continues:

https://tass.com/economy/1631715

13 June 2023. Novatek obtains patent for LNG technology with production capacity of 6 mln tons per year.

https://tass.com/science/1587231

10 March 2023. Roscosmos to go ahead with research into LNG-fueled rocket Amur.

https://tass.com/economy/1587199

10 March 2023. Sinara dealing with high-speed train development — CEO. Trains to move up from 250kph to 400 kph.

https://tass.com/economy/1595561

28 March 2023. Russia fourth in world in composite production: Rosatom CEO.

[This is important for civil aircraft production.]

https://smoothiex12.blogspot.com/2023/03/about-composites.html

28 March 2023. More on civil aviation: MS-21 etc.

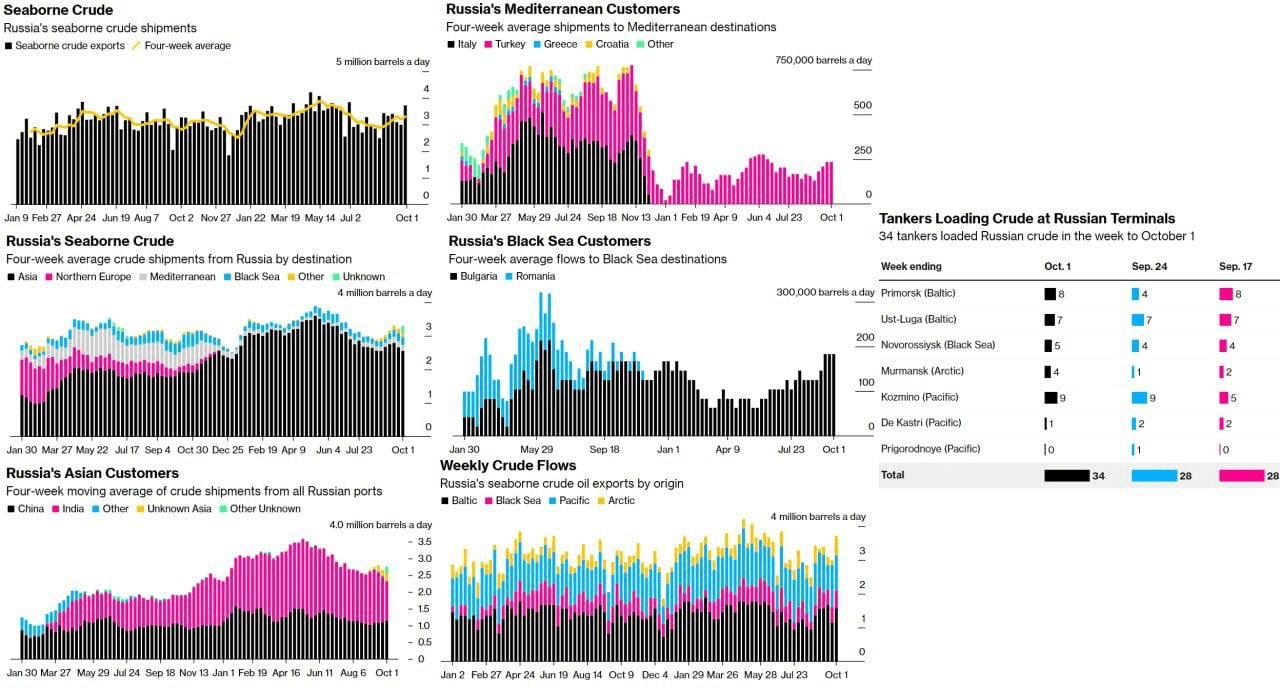

Yet despite sanctions, Russian oil and gas exports continue, albeit generating a lower income early in the year:

https://tass.com/economy/1568043

27 January 2023. Turkey’s energy ministry expects gas hub to start operations within a year.

https://tass.com/economy/1569541

31 January 2023. China’s growth in oil demand to sustain crude prices at $95-110 per barrel, experts say.

https://tass.com/economy/1578005

17 February 2023. Gazprom completes 88.15% of Amur GPP.

https://tass.com/oil-gas-industry/1590641

23 March 2023. Gazprom delivering 39.4 mln cubic meters of gas to Europe through Ukraine via the Sudzha pipeline. [per day.]

https://www.zerohedge.com/energy/eu-ban-russian-fuel-leads-diesel-glut-asia

26 March 2023. OilPrice.com

https://tass.com/economy/1595697

28 March 2023. New sanctions against Russia’s fuel and energy complex possible — Novak.

https://tass.com/economy/1595693

28 March 2023. Szijjarto, Novak discuss seamless delivery of Russian oil and gas to Hungary.

It is worth noting that oil exports continue to provide important revenue for the state budget, albeit at a lower level than before sanctions:

S, 3 October 2023:

What is happening to Russia’s offshore oil exports?

Well, nothing much. It just jumped to its highest level in three months. About 3.72 million barrels a day were shipped out of Russian ports last week. That’s 24% more than the week before. In previous weeks, shipments from Kozmino and Primorsk were reduced due to repair work.

The combination of soaring exports and rising prices has boosted the Kremlin’s revenues from oil export duties, which hit a new annual high last week and rose to their highest level since mid-January.

Already traditionally this year, the vast majority of supplies are going to Asia, where they are split between China and India.

A little more goes to the Black Sea and the Mediterranean Sea. In the former, Bulgaria picks up the cargo, and Turkey in the latter [end.]

Despite these positive signs, the issue of the state ignoring some pollution issues remained:

20 April 2023.

Russia responded to these hazards related to sanctions by attempting to increase economic cooperation with allies, and reassuring itself that the US could not have influence on Russian banks.

https://tass.com/economy/1595689

28 March 2023. Drafting of Sino-Russian economic cooperation plan already underway — deputy PM.

https://tass.com/economy/1587993

13 March 2023. US has no channels of systemic influence on Russian banks, markets — ACRA chief.

Growing importance of the Far East of Russia

https://tass.com/economy/1665841

This has been true for a few years now, and this is becoming increasingly recognised in foreign attendance of the Far East Economic Forum, particularly after the one in September 2020. That one was attended in person by Putin, Modi and the Presidents of Mongolia and Kazakhstan, with President Xi attending virtually. Among the decisions then were the re-routing of the Power of Siberia 2 gas pipeline through Mongolia, which would be permitted to charge transit fees, and which would reduce its consumption of coal. It was agreed to build a Russian nuclear power station in Kazakhstan, thereby alleviating an unnecessary energy shortage there while permitting it to continue exporting natural gas. India agreed to contribute to the construction of a large new shipbuilding yard near Vladivostok in which Indian ships for the Northern Sea Route [NSR] would also be built.

Attendance at the Far East Economic Forum was far greater this year, and the policy introduced a few years ago for granting special economic and tax concessions to various cities in the Far East seems to be encouraging growth, which is mostly of high-tech industry. This growing importance of the Far East of Russia can be seen in the geographical distribution of the Russian population below.

Population

The Russian population is on a slightly declining trend, with a birth rate (especially of ethnic Russians) lower than the government would like.

https://tass.com/society/1562139

13 January 2023. Natural population loss rate is down compared to 2021.

In addition, tens of thousands have left the country in protest at the SMO. This declining trend will have been partly offset by the refugees (at least 2 million) from Ukraine, as well as the incorporation of 4 southern and eastern Oblasts/Regions of Ukraine. The Russian Federal Statistics Service [Rosstat] gives a de jure picture of the Russian citizen numbers as of 1 January 2023, as well as other economic indicators on its home page:

The resident population estimate is 146,447,400 people. It also shows a graph covering the period from 1 January 1993 to 1 January 2023. Some of the recent increase visible on the graph is perhaps immigration of refugees who have taken Russian citizenship since the start of the SMO. Another interesting source is this:

https://populationstat.com/russia/

This interesting website also gives the population of the 20 largest cities in Russia, and points out that immigration (mostly of ethnic Russians) from neighbouring formerly Soviet countries is probably not as high as had been hoped for. The fact that 17 to 20 per cent of the population have expressed a wish to leave the country will have been worrying for the government, but this sentiment may have been drastically changed by the SMO, given the rampant Russophobia promoted by the Western media.

Life expectancy has risen, but the population is forecast to keep declining slightly. The implication of this for the dependency ratio implies that the retirement age should eventually rise, but a recent attempt to do this (when combined econometric and demographic modelling showed that it would have a detrimental effect on economic growth) led to a rapid modification of the proposed legislation. Any future attempt to raise the retirement age will presumably be made with greater caution.

The population data are updated on a daily basis here:

https://countrymeters.info/en/Russian_Federation

The geographical distribution of the population density can readily be assessed here:

{kind=link}

Income Distribution

One problem in analysing this evidence is the fluctuating exchange rate between the Dollar and the Ruble, but this source at least suggests that household incomes have been rising in recent years:

https://www.ceicdata.com/en/indicator/russia/annual-household-income-per-capita

This data set shows relative income and wealth levels:

One can click on the graphics to see a larger version. These indicate considerable inequalities of income and especially wealth, with the latter inequality being among the highest in the world. In my view this is an ongoing legacy of the 1990s, and growing the economy and rising real incomes for the majority of the population will probably remain a higher priority for the foreseeable future, rather than reducing wealth inequalities. That wealth is being encouraged by the government to take over companies abandoned by foreign corporations, but some Turkish corporations are also doing this (for example with MacDonalds franchise outlets, which have been rebranded as ‘Tasty, That’s It’ in Russian). This process is also being used to encourage ‘de-offshorisation’ of Russian capital, and this can be seen for example with new investment in agriculture.

Agriculture

One of the precipitating factors in the crisis that led to the end of the Soviet Union in August 1991 was its inability to pay the USA for its imports of chickens when immediate payment was demanded.

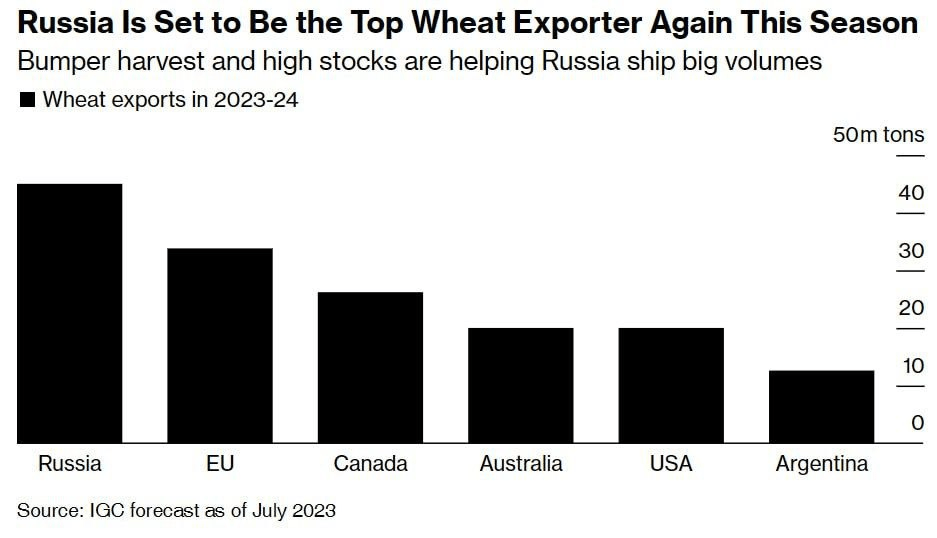

The situation in post-Soviet Russia began to change radically in 2014 when the results of a wheat cross-breeding programme that started in 1934 were completed. This 70-year programme resulted in 4 new varieties of winter wheat which did not have the disease known as ‘wheat rust’ and which could grow in poor quality soil in winter conditions. That meant that the sown area for wheat could be extended to completely new areas. Not only did this immediately help Russia withstand the sanctions that year owing to a rapid rise in exports, but it stimulated a series of policies designed to encourage mechanisation of agriculture and to diversify into other crops. These policies included reduced VAT and increased publicity for agricultural exhibitions showcasing new technologies. Consequently, when Brazil (under US pressure) reduced its exports of soya to China a few years later, Russia was able to step in and immediately supply 5 per cent of the Chinese soya market.

As is now well-known, Russia is a leading grain exporter and able to supply its domestic population with an increasing variety of other agricultural products. To illustrate the extent of this rapid change, in several recent years Russia has exceeded the all-time record wheat harvest for the Soviet Union, despite losing wheat production in Ukraine, Uzbekistan and Kazakhstan from its statistics.

Without going into the politics of the SMO grain deal agreed with and then broken by Ukraine and its Western mentors, it is worth noting that Russia is now the largest wheat exporter on the world market.

Ukraine’s exported wheat is now mainly produced by 3 American companies which have leased land to grow large quantities of genetically modified [GM] wheat. This amount of wheat seems to be less than that of Argentina, and much of it has remained within the EU this year, causing political problems from farmers’ protests in various EU countries.

Owing to sanctions, Russia is now planning to build its own fleet to export its wheat and other agricultural products. This could dramatically increase exports.

S, 20 June 2023:

Chronicles of “working” sanctions

Russia is building its own bulk carrier fleet to export agricultural products.

To: 1. not pay for shipping to foreigners; 2. deliver food around the world more efficiently.

The launch of the first domestic bulk carrier is scheduled for 2025-2026. There are plans to produce two or three Handysize and Supramax dry bulk carriers annually.

For reference: at the end of 2022 Russia became the world’s largest exporter of wheat. In addition, it increased the supply of flour, frozen fish, sunflower oil, confectionery products, meat and animal feed. According to Agriculture Minister Dmitry Patrushev, over the past 12 months, Russia has supplied food abroad for nearly $42 billion. And after the creation of its own bulk carrier fleet, the volume of supplies will increase several times over. [end.]

It is worth noting that while Russia is now self-sufficient in poultry, there is still an issue with dairy production:

https://tass.com/economy/1565081

20 January 2023. Russia may become self-sufficient in dairy production in 3-4 years.

This commentary below shows how funds located in tax havens are now being repatriated owing to rigorous enforcement of sanctions, which is resulting in de-offshorisation, increased import substitution and in this case, expansion of Russian agribusiness into formerly Ukrainian Regions:

https://johnhelmer.net/apples-tomatoes-the-sports-club-oligarchs/#more-70777

1 March 2023. In other words, this exemplifies how sanctions can be counter-productive.

Here are a couple of other detailed examples of how agriculture is being restructured rapidly under sanctions.

17 April 2023.

https://johnhelmer.net/in-the-seeds-war-who-is-burying-whom/#more-87890

25 April 2023.

Russian National Funds

In addition to the financial reserves held by the CBR, it is important to describe, however briefly, various other funds under direct or even indirect government control to help explain how an economy which is not in debt can build up reserves which enable it to absorb external shocks. These funds have probably been built up in response to the Russian default of 1998, which was caused by the Asian financial crisis of 1997. That default doubtless contributed to a growing movement to reverse the policies of the 1990s in important respects in order to re-establish Russian economic independence.

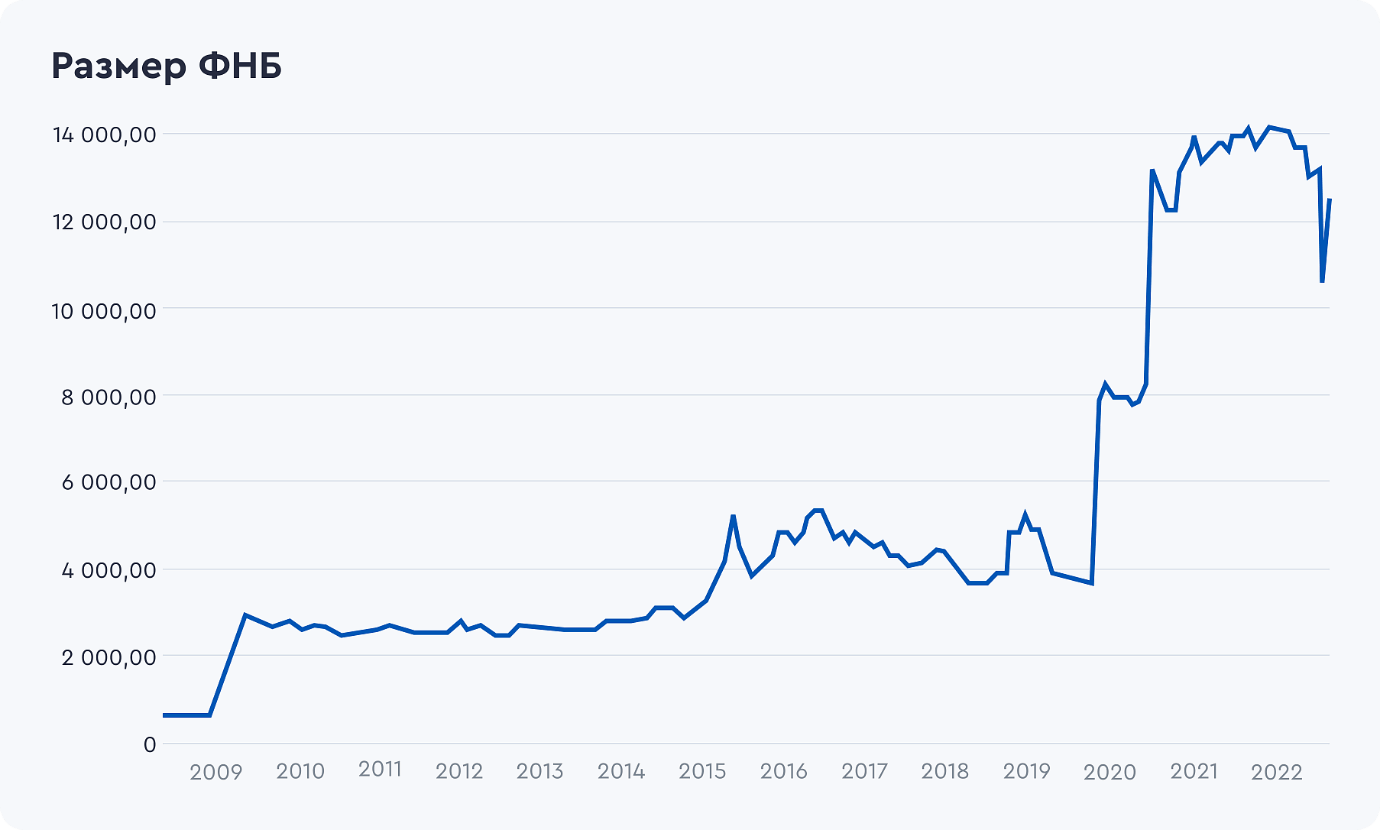

This is an important factor in explaining the resilience of the Russian economy: it is not in debt, unlike any other major economy, and so can deal with capital outflows without an immediate crisis. Various government-owned funds can be used either to foster growth or to stabilise the economy in adverse circumstances. For example: the volume of Russia’s National Wealth Fund as of 1 September 2023 reached $139.98 billion.

https://tass.com/economy/1670729

6 September 2023. For a historical account of the development and purposes of this fund, see:

https://en.wikipedia.org/wiki/Russian_National_Wealth_Fund

This source points out that there was an additional fund that was run down and closed in 2017. Presumably this helped the Russian economy to withstand the sanctions of 2014 and recover quickly by maintaining normal government spending and investment.

The above text also gives the figure for 1 September 2023 as being $142.8 billion. For present purposes, one can ignore this discrepancy between this text and the TASS report above and treat the figure as being $140 billion for September. It is clear from another table in the Wikipedia page that there were withdrawals in October 2022, and January and March this year to cover the federal budget deficit. These were fairly unusual withdrawals presumably consequent on the SMO, since the federal budget is not usually in deficit, but it is proposed to continue to run such a deficit for some months into 2024.

In February, it was decided to remove the Euro currency from the National Wealth Fund:

https://www.globaltimes.cn/page/202302/1285209.shtml

10 February 2023.

Russia’s de-dollarisation policy will be discussed below, but this is evidently part of it.

Russian Finance Ministry on the National Welfare Fund:

“The National Welfare Fund is a part of the federal budget funds subject to separate accounting and management in order to ensure co-financing of voluntary pension savings of citizens of the Russian Federation, as well as ensuring the balance (covering the deficit) of the Federal Budget and the budget of the Pension Fund of the Russian Federation.”

“On the first of September 2023 the size of the Fund was 13, 703.6 milliard Rubles. It gets its funds mostly from hydrocarbon revenues, when they are above the planned price, plus the income from management of the Fund by the Ministry of Finance. … It is also used for the purpose of increasing the effectiveness of the management of the State financial resources.”

The following commentary in Russian has a graph showing that the National Welfare Fund has grown almost 14 times from late 2008 to 2022, from 783,31 to 10, 774,98 billion Rubles in July 2022.

https://gazprombank.investments/blog/bonds/national-welfare-fund/

In July 2022, this fund amounted to $210.62 billion, being 15th in the world rating.

https://tadviser.com/index.php/Article:NWF_(National_Welfare_Fund_of_the_Russian_Federation)

History of investment spending.

Social Fund of Russia.

“The Pension and Social Insurance Fund of the Russian Federation is an off-budget state fund established by Federal Law No. 236-FZ “On the Pension and Social Insurance Fund of the Russian Federation” dated 14.07.2022, through reorganization of the Pension Fund of Russia and its merger with the Social Insurance Fund of Russia.

January 1, 2023, is the Fund’s founding date.

The Social Fund of Russia (SFR) aims to provide pensions, pension insurance, mandatory social insurance in case of temporary disability and in connection with motherhood, mandatory social insurance against accidents at work and occupational diseases, social security, and the provision of social protection measures (support) to certain categories of citizens.

The government of the Russian Federation exercises functions and powers of the SFR founder.”

Since this is stabilised using the National Wealth Fund, I am not treating this as an additional government asset.

Russian Direct Investment Fund

https://www.rdif.ru/Eng_Index/

The Russian Direct Investment Fund amounts to over 2.1 trillion Rubles, of which 1.9 trillion Rubles has come from co-investors, partners and banks. It has $10 billion of reserved capital under management. This amount may be used effectively but it is trivial in relation to the potential increases in foreign direct investment and in domestic investment funds from various state-owned giant corporations.

Gazprom and Rosatom

There are various state-owned corporations that have enormous resources combined with considerable engineering and research capacity but whose own financial reserves could in principle be used to secure wider or more immediate state objectives. These are called ‘national champions’.

Gazprom, the hydrocarbons corporation which owns its own bank, is one such potential source of funds supporting state strategy. For example, Gazprom has recently bought an entire supermarket chain that was previously under foreign ownership. Its reserves of natural gas are enormous, as can be seen below.

https://en.wikipedia.org/wiki/Gazprom

https://tass.com/economy/1578015

17 February 2023. Gazprom’s reserves ‘astronomical,’ leave other countries in the dust, says Putin.

https://tass.com/economy/1584695

3 March 2023. Gazprom buys out Shell’s stake in Salym Petroleum Development. Yet in general Russia’s oil policy is to reduce oil production in agreement with OPEC in order to maintain oil prices. This is in response to the West’s earlier attempt to put a cap on Russian oil prices:

https://tass.com/economy/1569575

31 January 2023. Factbox: Russian oil exports and West’s attempts to put a price cap on it.

https://tass.com/old-economy/1598195

2 April 2023. Russia to extend oil production cuts by 500,000 barrels per day until year end — deputy PM. This policy of raising oil prices by restricting OPEC Plus production (including Russian production) seems to be working recently:

https://tass.com/economy/1684291

4 October 2023. “Russia’s oil and gas revenues up 15% in September. The increase in September revenues was mainly due to the mineral extraction tax, which brought 1.087 trillion rubles ($10.9 bln) to the Russian budget (up by 24% compared with August).” These are all revenues, not just those of Gazprom.

Novatek is a notable private company in Liquid Natural Gas [LNG] production and shipping.

Rosatom

https://en.wikipedia.org/wiki/Rosatom

This vast state-owned corporation is responsible for the Northern Sea Route [NSR] near the Arctic coast of Russia (from the above link):

“The development of the Northern Sea Route has become a Rosatom priority after the company was appointed its infrastructure operator in late 2018. Rosatom seeks to organize ship navigation within the NSR, develop the infrastructure of seaports, including energy, create a navigation safety system, as well as navigational and hydrographic support. In addition, several Rosatom entities are involved in the development of international transit sea freight traffic along the Northern Sea Transit Corridor. Key companies include FSUE Atomflot, Directorate of the Northern Sea Route, Rusatom Cargo.”

The relatively new Military District that has been created for the Arctic seems to entail close cooperation with Rosatom which has overall operational control for civilian matters. Thus not only its financial reserves but its research and innovation expertise and its operational role make Rosatom a vital component of the Russian economy.

Overall, this close relation between the state and both state-owned and private corporations seems to work in terms of promoting well-founded resilient economic growth and the ongoing diversification of the Russian economy.

De-offshorisation and de-dollarisation

In addition to encouraging offshore funds to return, Russia has made it difficult for foreign companies to wind up their business in Russia, at least until a new buyer can be found. To some extent, this is reversing the earlier loss of political power by owners of large companies, since the state needs to negotiate with them to encourage them to take on former foreign-owned companies.

S, 28 March 2023:

Financial Times: About 2,000 foreign companies are waiting for permission from the RF Ministry of Finance to sell their Russian assets. The commission of the Ministry of Finance meets three times a month and considers no more than seven applications in one meeting. At this rate, it could take eight years for all applications submitted to be reviewed. According to analysts, only 206 foreign companies have completely sold their Russian assets. Those who seek to sell a business in Russia are constantly faced with new restrictions. [end.]

https://tass.com/economy/1559743

9 January 2023. Russian business quickly fills vacated niches: Kremlin.

It was reported earlier that 75.9% of foreign companies remain in Russia and the ones that left suffered very giant losses.

https://tass.com/economy/1597899

31 March 2023. Toyota motor plant in St. Petersburg transferred to Russian state.

De-dollarisation has advanced through a series of bilateral deals to pay in national currencies:

https://tass.com/economy/1572091

6 February 2023. Novatek eyes payments in national currencies for LNG.

https://smoothiex12.blogspot.com/2023/02/no-comments-needed.html

9 February 2023. Russian economy. Use of Euro to be reduced to zero.

https://tass.com/economy/1577471

16 February 2023 Mongolian banks soon ready to accept Russian Mir cards.

https://tass.com/economy/1593087

22 March 2023. Ditching dollar opens new avenues for Russian financial system — experts.

From Intel Slava Z, 20 April 2023:

De-dollarization continues. Russia and Bolivia are switching to settlements in national currencies. Now Russia will accept the Bolivian currency – Boliviano. This is highly relevant in the light of Rosatom’s desire to take part in the development of lithium deposits in Bolivia. Bolivia has a huge potential in terms of developing lithium deposits – in terms of explored reserves of lithium, Bolivia is one of the leading countries in the world, which, given the importance of lithium for modern electronics, makes this country extremely important in the processes of economic transformation of the world.

[end.]

https://tass.com/economy/1596323

29 March 2023. Promoting Mir bank card system crucial for Russian-Indian ties, Moscow trade official says.

https://tass.com/economy/1624641

29 May 2023. Russia increases settlements with partners in national currencies — Lavrov.

S, 13 June 2023:

In Turkey, payment by SBP and cards of Russian banks has started 🔥

All payment systems are accepted – Visa, MasterCard, UnionPay, Mir.

Payments are made through the domestic system SigmaPay, which accepts rubles and then sends the money to a Turkish bank. Technically, all transactions take place in Russia, so no one will get pinched. [end.]

S, 4 October 2023:

The share of official foreign exchange reserves held in US dollars worldwide stood at 58.9% in the second quarter of this year, data released a few days ago by the International Monetary Fund showed, broadly unchanged from a 25-year low first reached in the fourth quarter of 2020.

Since the start of the SMO, which dealt another blow to the established order, dollar reserves have fallen 2.9 percent despite a jump in the value of the currency. At unchanged exchange rates, the fall would have been 6.6%.

In July, only about 30% of Russia’s export transactions were in dollars and euros, down from about 85% in early 2022, the Bank of Russia said in a report.

Indeed, some reserve managers have switched to the Chinese currency, a habit President Xi Jinping intends to promote. IMF data show yuan reserves have tripled since 2016.

Brazil has adopted it as a trading and reserve currency, and President Luiz Inacio Lula da Silva recently urged developing countries to diversify away from the dollar. Argentina, which has been left without dollars after large IMF disbursements, has resorted to exchanging yuan with the People’s Bank of China in exchange for greater adoption of the Chinese currency.

U.S. data shows China has reduced its holdings of Treasuries by 21% since January 2022.

Nevertheless, the shifts look surprisingly small. As Elsa Lingos, head of currency strategy at RBC Capital Markets, put it in a note to clients this week, “If this is de-dollarization, it’s happening at a ridiculously slow pace.” [end.]

Note: I have deleted that last paragraph of this report, since it fails to understand that repayment of dollar debts reduces the total amount of dollars in global circulation, and thereby has a similar effect to a tightening of monetary policy within the USA itself. Of course some dollars may not have been used to pay back debts, but simply exchanged with currencies of other countries, but this cannot be assumed to take place in every case.

Russian holiday travel patterns have shifted, with adverse effects on traditional destinations:

S, 29 May 2023:

🌍 Outraged in Europe – sanctions did not prevent Russians from traveling, – RadioZET

Anti-Russian sanctions were intended, among other things, to limit the ability of Russians to visit other countries, travel and change places of rest, but after almost a year and a half it turned out that the number of countries welcoming Russian tourists is only growing.

📝 “Instead of Europe, they choose exotic countries for recreation and the number of Russian tourists abroad is constantly growing. In addition, the list of countries willingly hosting guests from Russia is regularly updated,” writes the Polish edition of RadioZET.

📉 Some statistics:

▪️ in 2022, Russian tourists made about 22.5 million trips abroad compared to 19.2 million in 2021. In 2023, the numbers will be even higher;

▪️ Turkey, Thailand, the United Arab Emirates, the Maldives, and Egypt are among the leaders hosting Russians;

▪️ many countries simplify the visa regime with Russia. Thus, Sri Lanka, Morocco, and Thailand plan to open direct flights;

▪️ India, Burma, and Oman are planning to open direct tourist communication with Russia, using the example of Cuba and Iran.

🍒 Cherry on the cake: in the summer of 2022 alone, European resorts lost one billion euros each due to anti-Russian sanctions. [end.]

Education

Russia has a very successful education system, including at secondary level. For example, secondary school students always do extremely well at Mathematical Olympiads.

Comments on Martyanov open thread, https://smoothiex12.blogspot.com/ 28 April 2023:

More sour grapes from the Collective West: if you don’t like the results just ignore them!

“Schoolgirls from Russia won the European Mathematical Olympiad and got the highest possible scores, but did not make it into the overall standings.” [end.]

In the case of higher education, Russia has recently decided to withdraw from the Bologna standard, and to return to Soviet standards, which are considered to be higher ones. Efforts had been made to learn from higher education experience in other countries. Russia had been collaborating with Scottish universities on discovering that an international survey showed that Scottish graduates had the best general knowledge. Presumably this has now ceased with sanctions, but it is clear that in some areas of research, and not only in military technology, Russia is leading the world. Two examples are worth mentioning:

The most advanced research centre for the Chinese company Huawei is situated in Skolkovo Science Park near Moscow. That is presumably owing to Russian mathematical and physics expertise.

There are six different MSc specialist courses in quasicrystals at Moscow State University. This implies considerable mathematical and physics expertise in 5-way symmetry in 3-D space.

BRICS

As is well-known, the BRICS group has expanded recently, and this could have considerable economic as well as geopolitical implications. So it is worth examining a few of the measures that Russia is taking to promote BRICS and thereby to begin to restructure the world economy. These measures were not selected on a systematic basis, but are rather the result of searching for items relevant to the SMO itself. They are merely illustrative. There are plenty of analytical commentaries about BRICS to be found on the Web. These illustrations may help flesh out such commentaries, and show that the Russian government is serious about implementing pro-BRICS policies.

https://www.france24.com/en/business/20230822-size-population-gdp-the-brics-nations-in-numbers

22 August 2023.

EAEU/BRI

https://tass.com/economy/1571275

3 February 2023. Russia to focus on food security as chair of EAEU

https://www.youtube.com/watch?v=qe2GiD5fCQY

15 April 2023. Interview with new president of New Development Bank.

https://tass.com/economy/1564245

18 January 2023. Russia, Kazakhstan sign roadmap for gas cooperation.

S, 16 May 2023:

Russia and Iran will sign an agreement that will provide a railway connection from St. Petersburg to the Persian Gulf.

The agreement between Iran and Russia on the construction of the Rasht-Astana railway section will be signed during the visit of Russian Deputy Prime Minister Alexander Novak to Tehran on May 16, 17. This was announced on Tuesday by Iranian Ambassador to Moscow Kazem Jalali. [end.]

https://tass.com/economy/1684725

4 October 2023. International North-South Transport Corridor could be alternative to Suez Canal — VTB. [VTB is a major commercial bank in Russia.]

China

https://tass.com/economy/1577959

17 February 2023. Russia may become China’s largest gas supplier in near future — Gazprom.

The gas holding also highlighted Russia’s collaboration with Turkey.

https://www.indianpunchline.com/us-paranoid-about-russia-china-summit/

19 March 2023. MK Bhadrakumar.

S, 23 May 2023:

Russian Prime Minister Mikhail Mishustin arrives on an official visit to China.

The head of government begins his visit by visiting Shanghai, where he will take part in a Russian-Chinese business forum and visit the petrochemical research institute of China’s National Petrochemical Corporation Sinopec. A meeting with representatives of the Russian business community working with the PRC is also planned.

In addition, a meeting is planned in Shanghai between the Russian prime minister and Dilma Rousseff, president of the New Development Bank of BRICS. From Shanghai, Mishustin will travel to Beijing for official talks with the Chinese leadership: he is scheduled to meet with President Xi Jinping and to hold talks with Premier of the State Council of China Li Qiang, with whom Mishustin will meet in person for the first time. Following the talks, a number of bilateral agreements are planned to be signed. [end.]

Prime Minister Mishustin is essentially presenting the Russian economy in China technically and beautifully – low inflation and unemployment, high production volumes, optimal tax regimes, digitalization of administrative services, etc. [end.]

Premier Mishustin’s speech is essentially programmatic for the construction of Russian-Chinese trade and economic relations:

Machine tool construction, civilian unmanned systems, shipbuilding, timber industry – promising sectors of cooperation with China

Strategic directions: power engineering and, in particular, nuclear power.

Trade turnover of agricultural products has increased by 40%, reaching $7 billion.

We are interested in developing transport corridors to China – through Kazakhstan and Mongolia. Expanding air links and developing the potential of the Northern Sea Route. [end.]

Amy Hawkins.

https://tass.com/economy/1622355

24 May 2023. Russian Export Center working on new support tools. [Oriented towards China.]

S, 31 May 2023:

Russian banks connect to the “Chinese killer” SWIFT.

30 Russian banks have already joined the CIPS payment system. Dozens more are awaiting approval of applications. It is expected that due to the transition to the analogue of SWIFT, logistics and settlements will become more predictable.

📝 “The main problem with payments is that they do not go through or go much longer than we would like. Within the framework of CIPS, there will be no such problems, ” said Georgy Mikhailets , partner of the Payments and Transfers company.

📈 Fast and accurate payments are also required by the growth of trade between Russia and China. Over the past year, it has grown by almost a third, and 70% of transactions with Beijing are already carried out in national currencies. Also, more and more banks offer deposits in yuan. [end.]

25 August 2023.

India

https://tass.com/economy/1605395

17 April 2023. Russia’s TMH gets $6.5 bln contract to produce 120 trains for India.

S, 17 May 2023:

Russia for the first time became the second largest supplier of goods to India. Exports in Q1 2023 amounted to $15.5 billion, which is 4.7 times higher than in Q1 2022.

The first place among the suppliers of goods is still occupied by China, despite the reduction in exports by 15.4%. The UAE became the third supplier ($12.7 billion). The fourth is the United States, the fifth is Saudi Arabia. At the same time, imports of goods from India to Russia increased by a third, to $946.6 million. The total trade turnover grew 4.1 times ($16.45 billion). [end.]

Africa

https://tass.com/economy/1590957

19 March 2023. Russia to set up its leasing company in Africa – Industry and Trade Ministry.

https://tass.com/economy/1591417

20 March 2023. Russia wrote off $20 bln of African nations’ debts, Putin says.

In addition, the meeting between Putin and African leaders seems to have led to a series of bilateral diplomatic agreements in Algeria and Libya, and helped promote a military security agreement between Niger, Mali and Burkina Faso. Africa has definitely moved up the list of Russian priorities, as the new membership of BRICS indicates.

For an indication of the relative size of BRICS prior to the recent accession of new member countries, one can use the same IMF data as was used to elicit the relative sizes of the largest 8 economies above. From that same data set, here are GDP adjusted for PPP for the five BRICS countries, in trillions:

BRICS

China, People’s Republic of: 33.01

India 13.03

Russian Federation 4.99

Brazil 4.02

South Africa 0.99

For comparison, here are the G7 economies, excluding the EU as a whole, using GDP adjusted for PPP:

United States 26.85

Japan 6.46

Germany 5.55

France 3.87

United Kingdom 3.85

Italy 3.20

Canada 2.39

G7 Total: 52.17

By this standardised measure, BRICS was already a larger share of the global economy than the G7 before the new membership was accepted. There are other ways of estimating this, for example as a percentage of global GDP, but this is surely a clear indication that the economic centre of gravity is shifting away from the G7.

Conclusion

It seems that the IMF has ceased relying on Russian government data in forecasting Russian economic performance, and may not even have an accurate estimate of the size of the Russian economy. Despite this, it has been possible to obtain recent evidence on the Russian economy using Russian government sources. It is clear that even during the SMO, a conflict that has galvanised rapid structural changes including de-offshorisation and a rapid increase in military production, plus a shift in hydrocarbon exports to a greater reliance on India and China, the Russian economy has returned to growth and is continuing to innovate and diversify its activities.

It has been able to do this owing to various state funds, ongoing positive export performance, despite sanctions on hydrocarbons, and rapid policy changes to deal with emerging problems, including an ability to engage in major import substitution. It also benefits from the short supply chains that come from having most raw materials available within the country, coupled with a large industrial and agricultural base and a financial sector that is growing in size and sophistication. These features have enabled Russia to remain focussed on fulfilment of its strategic national and international objectives, including developing policies that support emergent international economic organisations and that reduce its dependence on the Bretton Woods institutions of 1944.

6 October 2023.

amarynth, this opus is why globalsouth.co is in a league all its own .🦋 your ability to glean the rubies & gold from the net’s outrageous drag of dross is heaven sent. thank you.